BudgetInMind is a financial software. It tracks your spending and provide you with an overall view of what you have and what your owe. To be effective, you need to understand a few high level financial concepts, such as what is a Balance Sheet or an Income Statement. You need to understand globally how your assets are modelized in a financial statement.

There are three major reports that we, individual, care about.

- The Balance Sheet, a snapshot in time of what you have and how you financed it.

- The Income Statement that describes the inflows and outflows to your accounts (what you earn, what you spend).

- The Cash Flow that tells you how all the transactions you make impact your cash in your various banks.

The Balance Sheet

The Balance Sheet tells you what you have - your Assets - and how you financed them - your Liabilities. Liabilities are sometimes confusing; you have the obvious debt in the Liabilities, but you also have what we call Capital Funds, which is a reserve of all the money you (as your own shareholder) accumulated over time and decided to use to buy goods or other immobilizations.

The balance sheet is very important. It tells you how your wealth is spread. You can see if you have too much of it in cash, in immobilized property (car, house, ...), if you have too much debt, if you still owe money to the IRS, etc...

On the Asset side, you have your bank accounts, your securities (stocks, ...), your account receivable (for instance the ESPP amount your Company still holds), your cars, your house. On the Liabilities side, you have your debts (to suppliers, to banks, to the State (taxes) ...), your Profit/Loss balance and your reserves.

In the example above, you have a total wealth of $203K distributed over $62K in cash, $21K in cars and $120K in house equity. But you are not the only owner of this wealth. You only own $95K, the remaining $108K are owned by your bank(s)!

The Income Statement

The Income Statement is the record over a period (month or year) of all the inflows and outflows you made. In other words, it records your Income and your Expenses to generate a Result, also called Profit or Loss.

The Income Statement tells you how you spent your money and if you have managed to save some of it to achieve your long term goals.

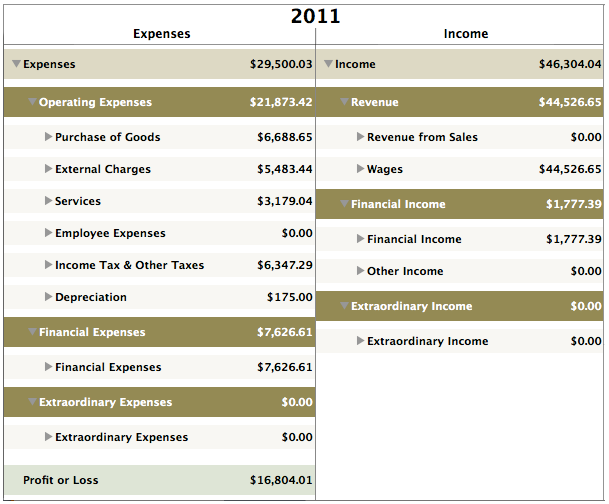

In the example above, you have earned $46K, mostly in wages ($1.8K in interests or dividendes), and you have spent $29K included $7K of debt servicing fees. You made a profit of $17K.

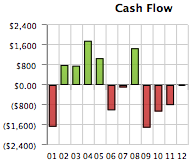

The Cash Flow Statement

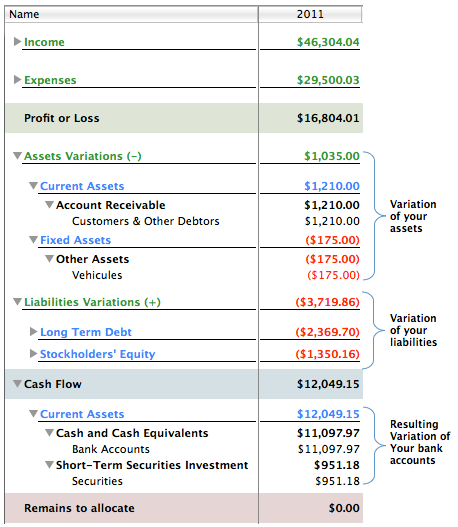

According to the example above, you earned $17K. But did you really see your bank accounts grow by $17K? Probably not.

There is one thing that the Income Statement doesn't show you: money that transferred between accounts in the Balance Sheet, that are not captured in the Income Statement. One of the striking example is debt. Indeed, when you make your monthly house debt payment, a portion of it is interest (and goes as an expense in the Income Statement) but the other portion is the reimbursment of the principal of the loan, that is a transferred from your bank account to the debt account, reducing the remaining debt by this principal amount.

So you may feel that your gained $17K, but in practice, how much of these $17K went to the reimbursment of debt? This must be tracked, and is the purpose of the Cash Flow Statement.

In the example above, the $17K profit was used to finance $1K variation in your assets, $1.3K variation in stockholder equity and pay back $2.4K of your debt principal, resulting in an increase of only $12K in your bank accounts.

Of course, you should follow your cash flow on a monthly basis (if not daily, looking at your bank accounts) since there can be large fluctuations month over month.